Veterans United Review [2024]

- Lowvarates.com Review - September 8, 2022

- USAA Review - August 16, 2022

- Veterans First Mortgage Reviews - August 5, 2022

When it comes to home loans, there are lots of options, but veterans, active-duty military, and spouses of service members should always look into their eligibility for a VA Loan. VA Loans have additional benefits than conventional loans, from more affordable mortgage rates to no monthly insurance.

Veterans United Home Loans, based in North Carolina, is one of the many lending companies that offer home loans to U.S. military veterans. We’re here to give a full Veteransunited.com review, covering pros and cons, customer reviews, and the kinds of loans Veterans United offers.

Table of Contents

About Veterans United Home Loans

If you’re looking for a Veteransunited.com review that’s covering how Veterans United works, whether it’s a real company (it is!) and it’s origination fees, you’re in the right place. Today, we’re talking all about Veterans United, discussing their loans, assessment, mortgage rates and fees, approval process, and more.

Veterans United Mortgage Loan Types

As a third-party organization, Veterans United facilitates several types of loans focused around VA Loans:

- Standard VA Loans

- Jumbo VA Loans

- VA Cash-out Refinancing Loans

- Streamline (IRRRL) Refinancing

- VA Energy-efficient mortgage

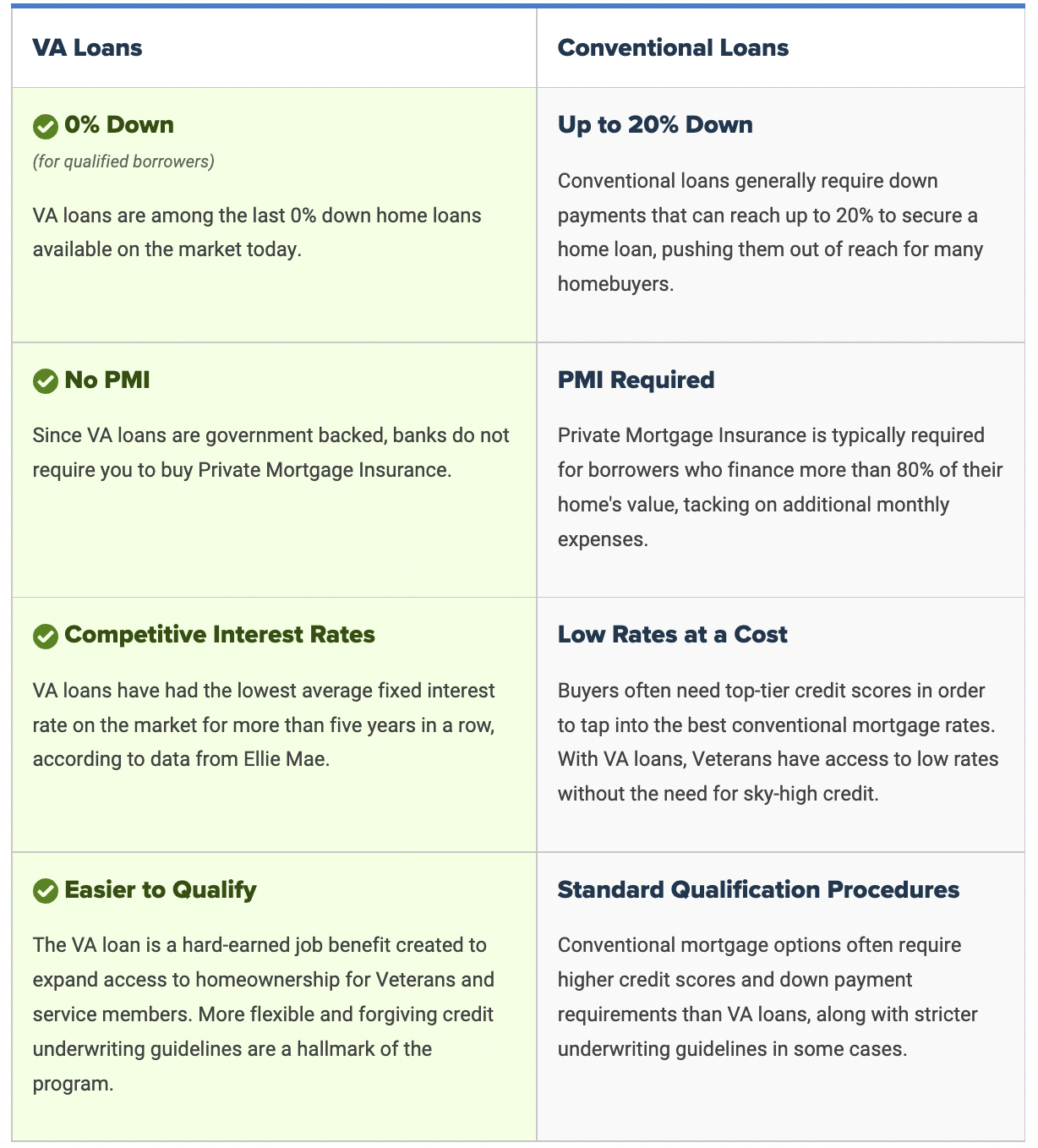

VA Loans are available to service members, veterans, and eligible surviving spouses. They include benefits such as not requiring a down payment or private mortgage insurance for getting a home loan, and obtaining loans for modifications. They also provide special benefits to Native American and disabled veterans.

Veterans United Home Loans Mortgage Rates and Fees

Since Veterans United is closely tied to the federal government-backed Veterans Affairs program, their interest rates are lower when compared to traditional home loans, as are their closing costs.

That being said, mortgage rates still vary based on your credit score, the house you’re buying, your loan duration, and the market conditions and regulations while you’re buying the house. The current rates are only valid temporarily, so you should make your buying decision only after researching the market.

At present, mortgage rates for a 30-year fixed VA purchase loan are 5.321% APR while that of a 15-year purchase loan is 5.499% APR.

As it goes with any normal lending procedure, your final payable amount will include some fees commonly known as closing costs or settlement fees. Most VA closing costs range from 3% to 5% of the loan amount.

Veterans United Application

Veterans United offers a 5-step process for VA Loan applications.

- Pre-approval: The pre-approval stage allows the lender to get to know you better. Here, you’ll typically be asked questions about your homebuying goals and your credit score and employment history will be assessed. You might also be asked to provide a couple of documents once your loan has been pre-approved.

- Home search: This is where the fun stuff starts happening. Veterans United will help connect you with real estate agents for the house search.

- Purchase contract: Once you’ve found a home you want to place an offer for, your agent will then help you choose a good price for the house based on the market conditions. They’ll also draw up a contract that includes contingencies up to closing.

- Underwriting: An underwriter will do a final inspection of your documents one final time. An appraiser will also assess the property to ensure that your final price is in line with the current market conditions and do not require necessary repairs before purchasing.

- Closing: Once you’re in the closing period, you’re just about done. Most buyers have a final walkthrough of the property and the lenders will assess your documents and the closing price one more time. Once all of this is done, you’ll be able to finish signing the final paperwork and get the keys to your home.

Like all the other lending companies that offer VA loans, Veterans United requires a preapproval from the U.S. Department of Veterans Affairs. It’s also sometimes called pre-qualifying. This lets the lending company know just how much you can afford to pay, so they would know how much to lend to you.

- Once that’s done, you should be ready to look for a new home and sign a purchase contract with the seller. After that, it’s all about the underwriting and closing.

Like all the other lending companies that offer VA loans, Veterans United requires a preapproval from the U.S. Department of Veterans Affairs. It’s also sometimes called pre-qualifying. This lets the lending company know just how much you can afford to pay, so they would know how much to lend to you.

Once that’s done, you should be ready to look for a new home and sign a purchase contract with the seller. After that, it’s all about the underwriting and closing.

Veterans United Approval & Closing Process

Closing day is when the seller, lending company, and the purchaser would sign all the paperworks related to the purchase. These papers include at least the following:

- Closing Disclosure: This is the final review of all the things to be exchanged during the buying process. It also includes how much the house is being sold for.

- Promissory Note: This is a contract between you and the lender. Because you will be buying the house through a va loan, this contract will detail how you will pay off the loan, its total cost, the mortgage term, and the interest rate.

- Mortgage Note or Deed of Trust: In case you can’t pay off your loan, the Mortgage Note or Deed of Trust lets the lender take the house when that happens.

- Warranty Deed: This is a deed that transfers the legal ownership of the property from the seller to the buyer.

- Report and Certification of Loan Disbursement (VA Form 26-1820): This tells the seller that the lender is going to pay them the required amount on behalf of the buyer.

- Request for Transcript of Tax Return (IRS Form 4506-T): This is a statement of your income and tax information. You may have to sign this a second time if your lender asked one from you during the preapproval process just to double check.

- Initial Escrow Account Disclosure: This tells how much you will contribute to your escrow account via your lending company so they could pay off your annual property tax and homeowner insurance bills. You won’t have to pay for it beforehand–the lender does this for you–but they need to make sure that they’ll be getting their money back when they do.

- Borrower’s Certification & Authorization: This is a certificate that gives the lending company access to your credit, tax, income, and employment records.

- Affidavit of Occupancy: Lastly, this states that you plan to live in the property that you are buying.

At Veterans United, most of the other important parts get done before closing day. This ensures a hassle-free purchase after preapproval. Many Veteransunited.com reviews cover how long after appraisal veterans united closes, which typically takes around 40 or 50 days until everything has been approved and ready for closing day.

Veterans United Review

Let’s review all you need to know about Veteransunited.com!

What to know about Veterans United Home Loans

Veterans United Home Loans is a lending company with over 28 offices over the United States, and has been doing so since 2002. As the name suggests, they mainly offer lending services for US military veterans. They do, however, also offer their services to those in active service as well as their families.

Veterans United uses a “My Veterans United” platform to help customers pay their mortgages easier, helping you remotely pay your loans, apply for new loans, and get in touch with the support team online.

Lenders should also be aware of the 2017 Veterans United lawsuit where the company was asked to pay $1.1 million against claims of overcharging their customers. These were loans that were largely backed by the U.S. Department of Veterans Affairs. The company has since stated that the issue had arisen from a since-addressed technical issue, and they voluntarily agreed to the settlement as a means of providing closure to those who were overcharged.

Veterans United Home Loans Pros

There are a few pros of going with Veterans United, such as:

- Transparent rates with few extra fees

- More than two decades of experience

- Provides supports with pre-approvals

- Overall positive customer reviews

With branches in all major states including Connecticut, Mississippi, Rhode Island, Pennsylvania, and North Carolina, getting your own Veterans United home is more straightforward.

Veterans United Home Loans Cons

While Veterans United is an established company, there is room for improvement.

- Current lawsuit over overcharging their customers

- VA Loans are not always the best fit for military members, and cannot be used by others

- There is no home equity line of credit or HELOC loans available

- There are new companies that have more updated loan providing services and practices

- While they say they do in-house pre-approval, what they mean is that they’ll guide you so you can get your pre-approval process, but they don’t really pre-approve in house

Fortunately, there are always alternative mortgage lenders to Veterans United to try if you don’t think Veterans United is the best fit.

Alternative VA Mortgage Lenders to Veterans United

Hero Loan

When it comes to servicing US military veterans, active-duty personnel, and their families, Hero Loan is one of the most straightforward yet unique lending companies. That is all because we personalize our services based on who’s asking for the loan and what they exactly need.

We also do the underwriting in-house, which means lower mortgage rates for you and no upfront or out of pocket costs—that includes the appraisal. At Hero Loan, there are never appraisal fees, or any other out-of-pocket costs.

How It Works:

Hero Loan offers more than just the regular VA Loan. Among these are:

- VA Streamline Refinancing

- Conventional Loan Refinancing

- VA Cash-Out Refinancing

- FHA Loans

If you can’t choose between them, you can just fill out your forms and their staff can help you choose. In fact, though qualifying for a VA home loan can require a lot of steps, our team lightens your load by helping with every step of the loan process, starting with getting your VA Loan Certificate of Eligibility. We do all the VA paperwork for you!

Another thing that makes Hero Loan so exciting is their closing period. While you usually have to wait for two months to close on your housing purchase, you can get that in just two weeks with our work.

Pros:

- Helps with pre-appraisal paperwork

- In-house underwriting

- Close VA Loans in 14 days

- No out-of-pocket fees or complex pre approval procedures

Cons:

- Services are for veterans, active personnel, and their families only

Hero Loan works best for when you’re starting out with your first purchase and you still don’t know the ropes. They’ll help you, and they’ll guide you. So why not try them out?

[Get Started with Hero Loan]

The Home Loan Expert

When it comes to super-fast lending applications, The Home Loan Expert is famous for their 5-Minute Loan Approval. And it’s just as they have advertised—you can get your loan application approved in five minutes.

In addition to VA Loans, these guys also offer a few other services:

- Adjustable-Rate Mortgages

- Bank Statement Mortgages

- Cash-Out Refinances

- Conventional Loans

- Debt Consolidation

- FHA Loans

The Home Loan Expert is great if you already know what you want. They have a lot more services than that, but you’re better off knowing what you want beforehand. After all, the long list of services can feel overwhelming if you’re new.

Pros:

- Home loan calculator

- Offers refinancing options

- Wide array of lending products

- House grants to accommodate disabilities

Cons:

- Too many options, can feel overwhelming for new borrowers

Ready to learn more? To find out what rates you could qualify for, start your 5-Minute Loan Approval* application right now!

Navy Federal Credit Union

Had too much to loan? Navy Federal Credit Union lets you have a 30-year mortgage even after you’ve used up all of your VA Loan benefits. And with 200 branches all over the US, they’re one of the larger mortgage companies out there.

With Navy Federal Credit Union, you can be eligible for a VA Loan, even if you’re not a family member of a Navy member on paper. You count as long as you live with someone who is. This is called the Military Choice program, and they open this for certain eligible US Navy members.

Another option could be the Homeowners’ Choice Loan, which is very similar to Military Choice. However, it’s made for people who are not eligible for VA Loans.

Navy Federal Credit Union also lets you refinance your:

- VA Loan

- Conventional Loan

- Military Choice Mortgage

- Homeowners Choice Mortgage

Navy Federal’s website has an easy-to-understand interface with facilities for online preapproval applications.

Pros:

- Opt for a no-down-payment mortgage

- Option to apply with alternative credit data

- A smooth and simple online application process

- More competitive rates compared to other mortgage companies

Cons:

- Certain loans like the USDA, FHA, home equity, construction loans, home equity line of credit, and reverse mortgages are not available

- Membership can be quite hard to obtain

- Does not include a VA Home Loan calculator

- You won’t be able to see the personalized rates before applying for the preapproval process

USAA

Unlike most of the companies in this list, USAA started out as an insurance company for military officers who want to get their cars insured. Now they offer a lot more options and have even expanded into offering VA Loans for military veterans.

Given their particular interest in military membership, USAA is quite well-versed in VA Loans. But they also offer other options like:

- A first-time homebuyer program

- Vacation financing

- Investment property financing

USAA’s VA mortgage does not need any down payment. You could basically just drop by, ask for money, and they’ll set you up for a loan as long as you have the right papers. But you may have to keep some cash for the closing costs.

Additionally, if you get a VA Loan from USAA, you won’t need to pay an origination fee. This helps save on cash, especially when you’re just starting out your life outside the military.

Pros:

- Your mortgage application can be submitted online

- Offers insurance and other financial products

Cons:

Veterans United FAQs

Is Veterans United affiliated with the VA?

Veterans United is not affiliated with any government agency, which includes the VA. However, they are VA-approved lenders.

Is Veterans United a real company?

Yes! Founded in 2002 in Columbia, North Carolina, Veterans United has been the leading VA Purchase Lender for six consecutive years. The company has several branches and has been licensed in all 50 states.

Is Veterans United a lender or broker?

Veterans United is a mortgage lender based in the United States that mainly facilitates VA loans. Mortgage lenders is a bank or company that offers and underwrites loans, while mortgage brokers are intermediaries between lenders and borrowers.

Veterans United Reviews on:

Besides the trusty Veterans United reviews that Google has at hand, you can check out more Veteransunited.com reviews from customers on these sites:

- Better Business Bureau (BBB)

- Credit Karma

- Consumer Affairs

- WalletHub

- Trustpilot

You could also check out a more business-centric Veteransunited.com review to get a better understanding of their company and business model if you’re planning to partner up with them.

Bottom Line: Is Veterans United a Good Lender?

Yes, Veterans United is a good, reputable lender on the surface. And there’s no doubt that they have a good name in the industry. Plus, their services are easily available, even to first-time homeowner veterans.

However, Veterans United can’t be the best all the time. So before you close on your deal with a certain lender, you may want to see how much the others would offer. Look and compare the rates, fees, and other parameters.

Hero Loan, for one, beats Veterans United when it comes to customizability. They offer refinancing so you could lower your rates. Plus, while online access is convenient, we offer both that as well as home loan officers in every state we’re in–so you can meet face-to-face with the local lenders that understand the community you’re into.