Am I Eligible for a VA Home Loan? | VA Home Loan Eligibility

- Lowvarates.com Review - September 8, 2022

- USAA Review - August 16, 2022

- Veterans First Mortgage Reviews - August 5, 2022

Being a homeowner is a prospect that understandably excites many people, and this is no different if you are a member of the armed forces. Whether you’ve decided that buying a home is a better option for you than renting one, or you’re simply looking for a place that you can return to after spending several years in active-duty service, this is where VA Home Loans, like the ones offered at Hero Loan, can help.

VA Loans are offered by many private companies to help active-duty service members, Veterans, and their surviving spouses finance a home purchase and are backed by the federal government. This is regardless of which branch of the military that they’ve served, including the:

- Air Force

- Navy

- Army

- Marines

- Reserves

- National Guard

While a Conventional Loan should still be considered, VA Loans have unique benefits that can appear almost too good to be true. In many cases, it’s a much better option and offers many advantages over a Conventional Loan, as it’s exclusive to those who have served our country.

If you want to begin the process, you can start by looking into the VA Home Loan eligibility requirements, and then start working with a VA Loan mortgage lender to find the best rates. At Hero Loan, we help you understand all the ins-and-outs of the VA loan process and work with you through every eligibility requirement–and do all the paperwork–so you can close in as little as 14 days.

Table of Contents

Who is eligible for a VA Home Loan?

VA Home Loans can be used by Veterans, active-duty service members (including National Guard and Reserves members), and surviving spouses. That said, your actual eligibility will be determined by the length of enlistment and your service-related duties. For veterans, depending on when you served, the amount of time required in order to meet qualifications for a VA Loan will vary.

Meanwhile, current enlisted service members must have completed at least 90 days of active-duty service, while National Guard and Reserve members must have at least six years of service. For documentation, you or your spouse must have a Certificate of Eligibility (COE) to show your lender before they can approve you for a VA Loan. This can serve as confirmation that you do qualify, based on your service.

VA Home Loan eligibility requirements include:

- Current duty status

- Length of service

- Manner of discharge

For those who are still active-duty members, their service history should include:

- At least a 2-year enlistment term for regular members

- At least a 6-year enlistment term if you are a National Guard or Reserve member

- 90 days of active duty during wartime

- 181 days of active duty during peacetime

Other considerations are whether you have a service-related disability, as it may affect the final decision on your VA Loan. Additionally, you must have or meet the following:

- Certificate of Eligibility (COE): Proof that you meet the VA’s requirements for a loan based on your service record. Surviving spouses must still apply for one should they be looking to secure a loan on their own.

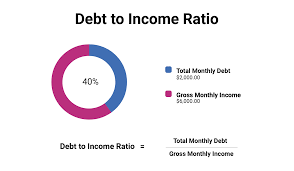

- Lending Requirements: While it will vary per individual and lender, a good credit score would be 620 and above. Additionally, aim to have a debt-to-income ratio (DTI) of around 41% to have the best odds.

How do I know if I’m eligible for a VA Home Loan?

Your VA Home Loan eligibility is determined by your time in active-duty service and if you have a COE to show as proof. If you were discharged before you met the service requirements, you may still meet the eligibility requirements if:

- You were discharged for hardship.

- You were discharged due to medical conditions.

- You were discharged due to a service-connected disability.

- You were discharged as an early out volunteer. (You must have at least 21 months in a 2-year term completed.)

- There was a reduction in force.

If you were discharged because of a service-connected disability, you might also be entitled to other benefits, such as:

- The VA Funding Fee exemption when securing a VA Home Loan

- The ability to count disability income depending on your disability rating

However, there are a few restrictions on who may get a VA Loan. For instance, you may not qualify for VA benefits if you have received a discharge that was Other Than Honorable (OTH), Bad Conduct Discharge (BCD), or a Dishonorable Discharge (DD).

How spouses can verify their VA Home Loan eligibility

If you are the surviving spouse, then you may meet the VA Home Loan eligibility requirements to receive a COE if the veteran is:

- Considered missing in action

- A prisoner of war

- Was killed while in service

- Died because of a service-connected disability

You will need to provide your marriage license as proof. However, you must not have remarried to be eligible. Or, if you did remarry, you didn’t get married before you were 57 years old. If you qualify and can get a COE, you will still need to meet any other requirements a mortgage lender may have.

VA Home Loan lender requirements

While there is no minimum credit score set by the Veterans Administration, some lenders may ask that you reach a certain credit score before approving you for a VA Loan.

This is typically around 580 or better, but that will vary per lender. Fortunately, you may still be able to get a VA Loan with a score of 500 and below, and having a lower credit score will not lead to risk-based pricing adjustments.

If you want to increase your chances of having your VA Loan application approved, you can take the following steps to help mitigate a bad credit score:

- Offer a bigger down payment. Depending on your income and how much money you can put as a down payment, it might be enough to overcome any hurdles resulting from a bad credit score.

- Improve your credit score. This is the most direct way of improving your chances of having your application approved, and you can begin by requesting a credit report that can help outline what you need to do to get started.

- Have a co-signer. A co-signer with a better credit score will ensure you can repay a mortgage loan if you default on your loan, improving the odds that you qualify for one. But for a VA Loan, the co-signer must be a spouse or another eligible service member.

- Improve your debt-to-income ratio (DTI). Your DTI measures your ability to manage your monthly payments. You should aim to have a DTI of at least 43% to improve your chances of a lender approving your application.

One reason you might be denied a loan is that your property might not meet minimum property requirements (MPRs). An appraiser will conduct an inspection to ensure your home is structurally sound before you can be approved, which can make VA loan appraisals more challenging. Lenders may also have additional requirements you may need to meet to be approved for a VA Home Loan.

Best VA Home Loan Lender Options

Hero Loan

Hero Loan is one of the fastest-growing loan financing companies, and it proudly specializes in serving veterans, active-duty service members, and their families across the nation. They understand the needs of veterans and military members, so they provide personalized services to ensure you are comfortable throughout the process and feel supported.

Hero Loan is also endorsed by the VA, making them a great lender to work with in securing a VA Loan to finance your home purchase. They can close a deal in as little as 14 days, providing lower mortgage rates without upfront or out-of-pocket costs, including the VA appraisal.

How It Works:

Hero Loan offers several different services depending on your needs. In addition to standard VA Home Loans, they also offer:

- VA Streamline Refinancing (IRRRL)

- Conventional Loan Refinancing

- VA Cash-Out Refinancing

- FHA Loan

You can begin the process by filling out your personal information and applying for the loan or service you would like to use. Before you know it, a friendly Hero Loan representative will reach out to you and will begin guiding you through the approval process.

Hero Loan will also help you determine your VA Home Loan eligibility and assist with any paperwork required to get your COE. If you have any questions about the process or alternative services, such as FHA Loans and Refinancing, they are there to help you.

Pros:

- Complete all VA paperwork for clients

- Underwrite all VA Loans in-house

- Can close VA Loans in as little as 14 days (compared to the two-month standard)

- No appraisal fees or out-of-pocket fees

Cons:

- Only services veterans, active-duty service members, and their families

The Home Loan Expert

If you are looking for a hassle-free experience and the comfort of working with experts who can guide you, then The Home Loan Expert has your back. Their online website is easy to navigate and offers a wide range of services, keeping things simple.

Unlike other companies that don’t serve veterans and active-duty service members, The Home Loan Expert works hard to help ensure every step of the process is as easy as possible in order to avoid any confusion. They also understand how stressful it can feel if this is your first time securing a mortgage loan and will happily guide you through the entire process, from start to finish.

You can begin the process online now to apply for a VA Home Loan by starting their 5-Minute Loan Approval* application.

Home Loan Expert’s helpful mortgage calculator!

How it Works:

Along with VA Home Loans, the Home Loan Expert also offer:

- Adjustable-Rate Mortgages

- Bank Statement Mortgages

- Cash-Out Refinances

- Conventional Loans

- Debt Consolidation

- FHA Loans

- First Responder Loan Program

In addition to the above, they offer other services you might consider, like the FHA Insured Loan and the USDA Home Loan.

If you have any concerns about any step of the process, their friendly representatives will guide you through it and answer any questions you may have. Additionally, if there’s anything that you need extra clarification on – such as whether you can have multiple VA Loans at a time, if you can use it on new construction or even manufactured home, you’re not sure about the appraisal process, or any other concerns about closing a loan – The Home Loan Expert is here to help!

Pros:

- Streamlined application process with quick approvals

- House grants can be used to accommodate a service-connected disability

- Offers a Native American Direct Loan program, should you need it

- Includes a VA Home Loan calculator

Cons:

- Can be challenge to decide which service to use with all their different loan offerings without any guidance

Veterans United Home Loans

Veterans United Home Loans is another major mortgage lender that can help you finance your home purchases. They specialize in working with veterans and active-duty service members and in addition to VA Home Loans, they also offer FHA Loans, USDA Loans, and Jumbo mortgages.

Veterans United can also help you determine which one will best suit your needs.

How It Works:

If you are looking to refinance a VA mortgage, Veterans United Home Loans offer you the choices of:

- VA Interest Rate Reduction Refinancing Loan (IRRRL)

- Cash-Out Refinance

Additionally, they allow you to apply for mortgage credit data, circumventing the need to use your primary credit data. This way, you can show that you can manage your bills on time, which is especially useful if you have a poor credit score, making them a great lender to work with.

Like other lenders, they can help you determine your VA Home Loan eligibility and help you through the process of closing on a loan.

Pros:

- Easy-to-use application online or at a local office

- Offers several different types of loans

- Will allow the use of other forms of credit in case you have a poor credit score

Cons:

- Does not offer some standard loans, such as a Home Equity Loan, Reverse Mortgage, or Construction Loan

- Personalized rates are not available online

Conclusion: Are You Eligible for VA Home Loan?

While it might feel overwhelming determining your eligibility for a VA Home Loan–and differentiating between all of the mortgage options. But the good news is that the knowledgeable team of experts at Hero Loan understand this–and that’s why they’re dedicated to helping you understand the entire process.

Their friendly professionals are eager to help guide you through determining whether you meet the VA Home Loan eligibility requirements and walking you through the steps of closing on a loan. Even if you have a lower credit score, they’ll work with you to find the best rates. To learn more, why not start get started on a fast and easy loan application today?