VA Mortgage Rates: Your 2024 Guide

- Lowvarates.com Review - September 8, 2022

- USAA Review - August 16, 2022

- Veterans First Mortgage Reviews - August 5, 2022

For veterans who are transitioning from active-duty service back into the civilian life, having your own home is one of those things that can help make the transition go much easier. Fortunately, the ability to purchase the home of your dreams has been made even easier, thanks to VA Home Loans, like the VA Loan and Cash Out Refinance options offered at Hero Loan.

Because they’re backed by the federal government, these VA Home Loans:

- Offer competitive interest rates

- Provide flexible qualifying criteria

- Can be used on any home

- Do not require any down payment

Getting a VA mortgage is one of the most popular options for veterans who, instead of renting, want to purchase their own homes and settle down in a community. Of course, mortgage rates can always fluctuate, so it’s important to know what the current mortgage rates are for VA Loans, how VA Loan rates are determined, and the steps you need to take to get a VA Loan.

Table of Contents

What are current VA mortgage rates?

VA Loans are supported by the U.S. Department of Veterans Affairs. That said, the mortgage rates are highly competitive and can change on a daily basis, depending on market conditions.

For instance, 30-year fixed VA rates currently have interest rates hovering somewhere around 4.25%–4.9% and annual percentage rates (APRs) between 4.56%–5.3%. Typically, all other types of VA mortgages fall into the percentages shown above for 30-year fixed rates.

The higher or lower rates you may get are also influenced by factors you can control, so you should always get a personalized rate quote from your VA Loan mortgage lender. That way, you can be confident you’re getting the best rate for your loan.

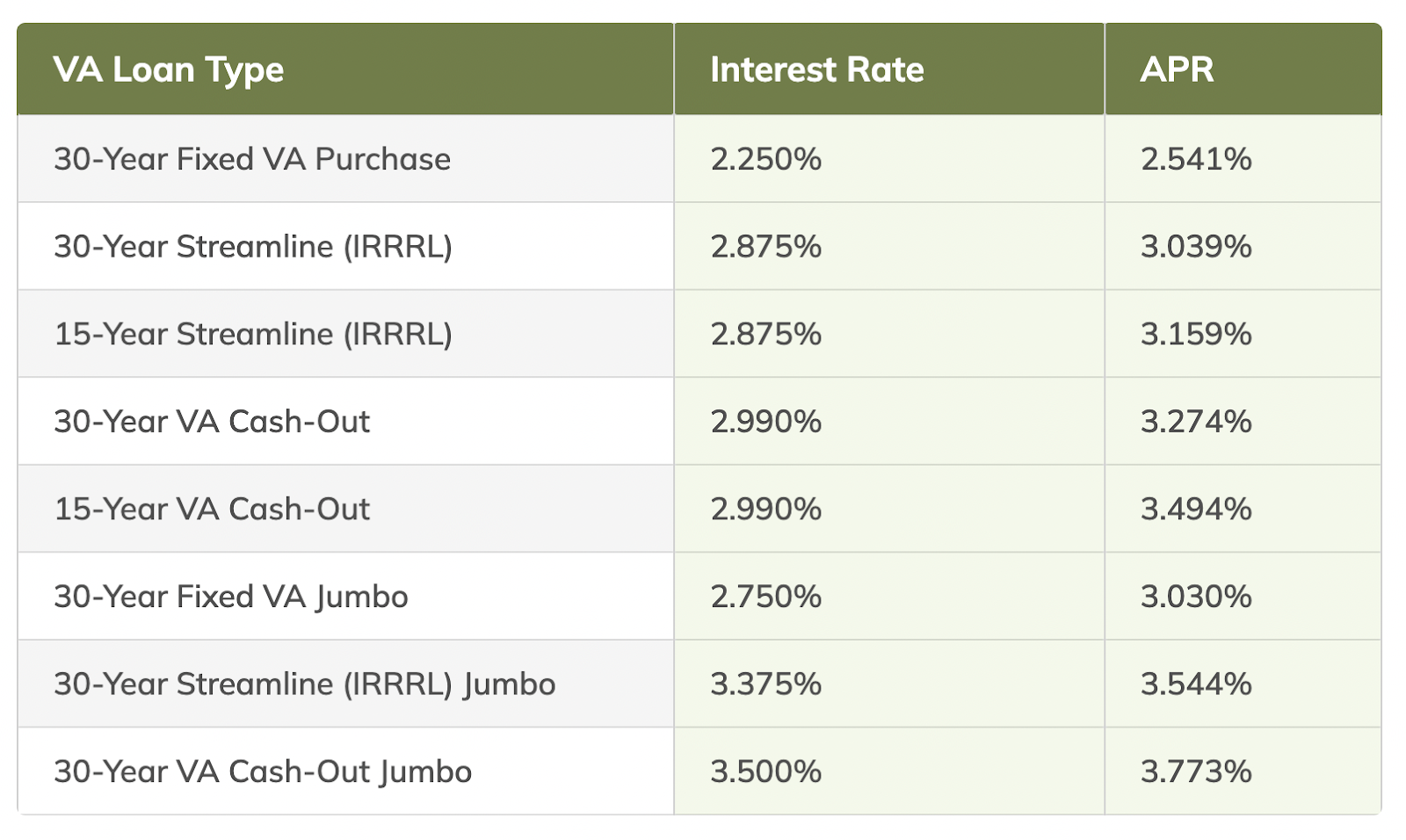

What are the current VA refinance rates?

Refinancing your existing VA mortgage is one of the more important financial decisions that you could make as a homebuyer, as doing so can help significantly reduce your interest rate and even allow you to secure reduced monthly payments.

However, many factors–such as the loan-to-value ratio, your creditworthiness, and even the type of VA Refinance Loan you want–will directly affect these VA refinance rates.

To help you better understand these finicky details, let’s go ahead and break down the current VA refinance rates by type. It is also good to note that all these rates change daily.

- Interest Rate Reduction Refinance Loan (IRRRL) or Streamline Refinance

- 30-Year Fixed: Interest Rates are at 4.500%, and Annual Percentage Rates are at 4.659%

- 15-Year Fixed: Interest Rates are at 4.375%, and Annual Percentage Rates are at 4.653%

- 30-Year: Interest Rates are at 4.500%, and Annual Percentage Rates are at 4.811%

- 15-Year: Interest Rates are at 4.375%, and Annual Percentage Rates are at 4.918%

- Jumbo

- 30-Year IRRRL: Interest Rates are at 4.750%, and Annual Percentage Rates are at 4.911%

- 30-Year Cash-Out: Interest Rates are at 4.750%, and Annual Percentage Rates are at 5.065 %

What is the lowest VA mortgage rate ever?

In recent years, mortgage rates have dropped significantly, proving through time that they could always get much lower. However, this isn’t necessarily set in stone, since there are many factors that contribute to the rise and fall of these rates.

The lowest mortgage rates were recorded during these years:

- 2012, with an average of 3.66%

- 2020, with an average of 3.10%

- 2021, with an average of 2.96%

According to Freddie Mac’s average summary running from 1971 through to 2021, you can see the first significant low of the average 30-year fixed rates in 2012. That year averaged an interest rate of 3.66%, which was barely revisited (until a couple of years ago)

U.S. weekly averages in the last 10 years.

When COVID-19 hit in 2020, the effects of the global pandemic led to the lowest rates ever recorded in the past 20 years. As the economy tanked, the Federal Reserve ensured that funds remained in circulation by forcing down the interest rates. According to Freddie Mac, 2020 had an average of 3.10%, with December of that same year averaging at a staggering 2.68%.

This went to influence the average of the year 2021, which was at 2.96%. Of course, these low rates are once again rising, but they’re still hovering fairly close to these record lows.

How VA Loan rates are determined

Even though the VA Loan is specifically for veterans and service members, the Department of Veterans Affairs doesn’t set the loan rates–they just guarantee the loans. Instead, private lenders are the ones who lock these rates in.

Before you can snag that quoted VA Loan rate, though, the following factors are usually considered:

- Your Credit Score. This is a very important factor, as it’s the one that helps lenders determine a personalized loan rate. Since VA Loans generally do not require clients to make a down payment, your creditworthiness goes a long way in getting you better rates.

When you have a credit score of 740 and above, you’re typically going to be first in line for the best rates possible. However, this doesn’t mean that lower credit scores get terrible rates–it just goes to show that higher credit scores can mean better VA Loan rates. - Your Loan Repayment History. Your loan repayment history is a record of your past borrowings. If you’ve always been on time while repaying your previous loans, this helps your credit score and will contribute to you getting lower loan interest rates.

- The Type of Loan. There are a few different types of VA Loans. They could be a Fixed-Rate Mortgage, an Adjustable-Rate Mortgage (ARM), refinance loans, and VA Jumbo Loans, among others. While the rates may not have that big of a difference, the type of VA Loan you apply for also contributes to your loan rate.

- Loan Duration. This is also referred to as the loan term. Generally, this is either a 30-year or 15-year term, but it could be lower. Lower loan terms usually can net you lower loan rates. However, due to the competitive nature of lenders, even the longer-term VA Loan rates are pretty easy and won’t be a thorn in your side.

Why are VA mortgage rates different?

Some borrowers don’t know this, but VA Loans are backed by the Federal Government’s Department of Veterans Affairs. This allows lenders the option of charging lower interest rates to active-duty service members, veterans, and surviving spouses.

Because of this policy, it generally brings the average VA Loan rates somewhere below the conventional mortgage loan rates, even when you add in the cost of the funding fee. The competitive nature of VA Loan lenders also makes these loan rates differ from each other, as well as personalized factors of each homebuyer (such as your credit score, for instance).

Plus, because VA Loans don’t require a down payment, you can start your home buying journey without needing to use all your savings.

Do veterans get better mortgage rates?

Normally, veterans, surviving spouses, and active-duty service members are eligible for these exclusive VA mortgage rates. Seeing as the availability of these loans was especially designed for them, they get to enjoy the benefits attached to VA Loans.

However, when applying for mortgages, you should always research the different types of loans to ensure that you get the best rates.

Not all VA mortgages may be applicable to the home loan requirements that a veteran or a service member might need, and the availability of them can vary. In such situations, a conventional mortgage may just be what you need. So while typically veterans do enjoy better VA mortgage rates, you may just find the perfect mortgage rate you require outside the VA mortgage program.

How to get the lowest VA mortgage rates

Finding extremely low VA mortgage rates can definitely be more than a bit tricky. This means that finding the lowest rates also requires that you put in a little legwork to help ensure that you get the best rate and aren’t denied your VA Home Loan.

- Fortify Your Finances. If you’re trying to get a loan, then this is one of the best things you can do. Since VA Loans are not much different from a Conventional Loan, higher credit scores will influence your mortgage rates. So increasing your credit, as well as making a sizable down payment, helps to secure a VA mortgage with a lower rate.

- Get Personalized Rates Quotes from Different Lenders. Sure, this does require some extensive market research on your part, but it’ll give you a better idea of the availability of these rates.You can push down your mortgage rates even further by requesting personalized quotes, as this can give you a more specific idea of what you’re eligible for. At Hero Loan, we make it easy for Veterans and military families to get the home loans they deserve–closing in as little as 14 days.

- Take Advantage of Discount Points. Discount points usually help to lower your personalized rates by allowing you to make a higher up-front payment. Sure, making a down payment or buying discount points means you’re putting some money down up front, but it also really lowers your interest rates in the long haul.

- Consider State Loan Programs. You may just be in a state that offers additional programs that assist veterans and service members. This may come as assistance to make the down payment, discount points, real estate agent services, or other benefits you may have no idea about. So, don’t hesitate to seek them out!

Source: Hero Loan

Who sets VA Loan rates?

As we’ve already established, contrary to popular belief, the Department of Veterans Affairs doesn’t set the VA Loan rates. Based on how the market flows, VA mortgage lenders actually set these rates. This is why you see different VA mortgage rates from different lenders.

This means that, as a great way to lower and reduce your interest rates, some lenders allow homebuyers to purchase discount points. This may seem like you are spending more at the start, but it usually pays off – especially for homebuyers who are going for the long-term options like 30-year fixed loans.

What credit score is needed for a VA Loan?

Having a good credit score poses so many advantages for anyone who is considering any type of mortgage loan. This is regardless of if you’re looking to purchase a primary residence, considering starting construction on a brand-new home, or looking for a second home.

But, unlike conventional mortgage loans, the Department of Veterans Affairs doesn’t have minimum credit score requirements for getting a VA Loan. In fact, a Conventional Loan typically has its minimum FICO score set at 620 and above. However, minimum credit scores for VA Loan borrowers are set by lenders, so you can easily find a lender that can accommodate your credit score.

Having said that, the higher your credit score, the lower your mortgage interest rate. If your credit score is 700 and above, you will be enjoying the lowest interest rates anyone could ever have on a VA mortgage loan.

On the other hand, while there isn’t any minimum credit score requirement imposed by the Department of Veterans Affairs, some lenders qualify clients who may have credit scores between 580–620.

Some may even allow credit scores that go as low as 500. These types of lenders will often pose some challenges for their clients to ensure that the entire system works in the favor of both parties, though, and you might need a co-signer in order to qualify. If you don’t want to apply for a VA Loan with a low credit score, you can try to find ways to improve your credit score, such as by maintaining low balances on your credit cards and making all your credit card payments on time.

Conclusion: The Best VA Mortgages Rates Today

As a veteran, you’re no stranger to pushing up your sleeves and tackling difficult tasks by yourself without hesitation. However, trying to get approved for a loan shouldn’t be one of those things. Instead, the experts at Hero Loan are here to make this task as easy as possible for you. After everything you’ve done to serve our country, they understand that it’s the least they can do for you.If you’re considering meeting a real estate agent and are ready to move forward with your home purchase, the friendly team of professionals at the Hero Loan can help you lock in your personalized interest rate, all within your financial means. To learn more, why not go ahead and get started on your loan application today?