VA IRRRL (Streamline Refinance) Loan Guidelines, Rates, and Programs

- Lowvarates.com Review - September 8, 2022

- USAA Review - August 16, 2022

- Veterans First Mortgage Reviews - August 5, 2022

The VA IRRRL loan — also known as a streamline refinance loan — is a fast and simple option for refinancing if you currently have a VA Loan. Just like all VA-backed loans, those who are eligible will receive competitive rates with flexible terms, and VA IRRRL loans offer lower interest rates and no down payment.

There are pros and cons to any loan out there, in this article, we will cover all things VA IRRRL so you can make the best possible informed decision when it comes to refinancing your home loan.

Table of Contents

What is a VA IRRRL Loan or Streamline Refinance Loan?

A VA interest rate reduction refinance loan or IRRRL is a VA-backed refinance loan for those who already have a VA loan. Also known as a streamline refinance, a VA IRRRL allows those who are eligible to lower monthly mortgage payments with a lower interest rate or change from an adjustable rate loan to a fixed rate loan.

While the IRRRL is not the only VA-backed refinance option, it is the simplest one. The other option is a VA Cash-out Refinance loan, where you have to calculate your loan-to-value ratio and then take out cash for the amount of equity that you have in your home.

So if a fast, easy refinance for a lower monthly payment is what you’re looking for, then the VA IRRRL could be the right choice for you.

How Does a VA Streamline Refinance Loan Work?

Essentially, refinancing means taking one mortgage and swapping it out for another that better fits your needs. There are several common reasons to refinance a mortgage, such as to tap into your home’s equity, get a lower payment, or change your mortgage term. For VA Refinancing, you are just refinancing a VA loan, not a conventional loan.

A VA IRRRL allows you to refinance your mortgage solely for a financial benefit. You can refinance for reasons like:

- A lower monthly payment

- A lower interest rate

- Changing an adjustable-rate mortgage to a fixed-rate mortgage

Note; you can’t refinance just because you just don’t like your current lender. It must provide some sort of improvement to your current payments or long-term costs. And, you can’t cash out through an IRRRL.

Am I Eligible for an IRRRL?

There are certain criteria that must be met in order to be eligible for a VA IRRRL. In order to obtain a VA loan, you must have already qualified as far as your eligibility as a service member.

This is where you obtain a certificate of eligibility (COE). Once you have the COE, you’ve proved your VA home loan eligibility for all VA-backed loans including the VA IRRRL.

After going through all of the steps to get the initial VA-backed loan, there are some additional requirements for the VA IRRRL

- You must already have a VA loan

- You must be refinancing your current VA loan

- You have to be able to certify that you live in or used to live in the home you are looking to refinance

Additionally, if you have more than one mortgage on the property already, the other lenders will have to agree to make the new VA IRRRL the first mortgage. When this is the case it is best to speak with the lender of the second mortgage prior to proceeding with the streamline refinance.

Why You Might Want a Streamline Refinance Loan

There are many reasons that people decide to refinance their current mortgage loans. It’s a matter of personal needs and preferences, and might include:

- Lower interest rates result in lower monthly payments

- Changing from a variable rate loan to a fixed rate loan

- You need to make upgrades to your current home

- Changing your mortgage term for smaller monthly payments

After living in your home for some time and making monthly payments you will have a better sense of what works for you and how to optimize your repayment terms to best suit your lifestyle.

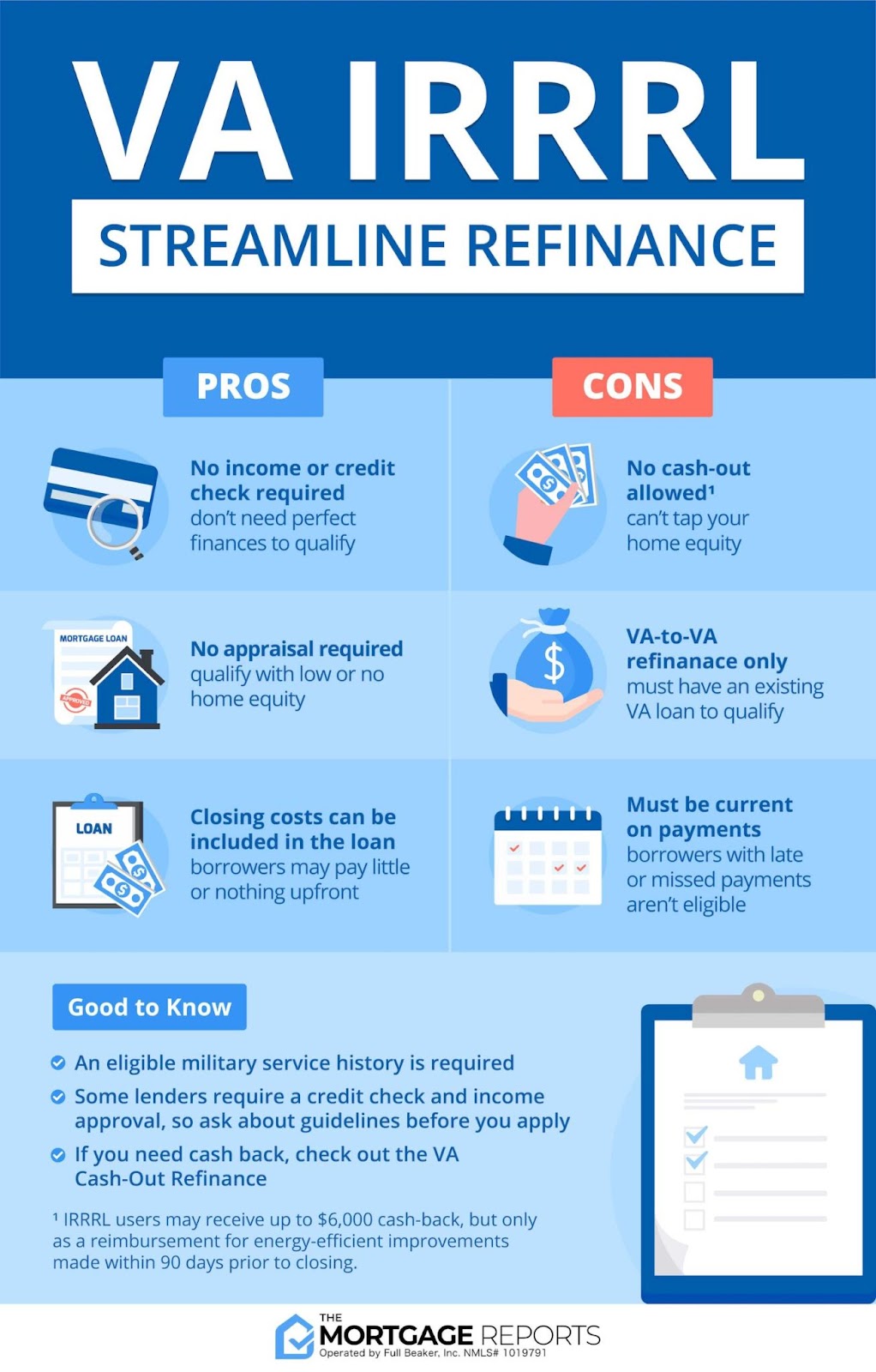

VA IRRRL Pros

When looking into a VA streamline refinance loan, it’s important to look at all of the potential benefits. With more than one refinance loan option available, having a comprehensive list of pros and cons for all of the loan types will help you decide which one is right for you.

Keep in mind that the VA IRRRL is going to offer the lowest rates out there. Be sure to check the current VA mortgage rates so you know you are getting the best rate available and if you are not, try a different lender.

Here is a list of the benefits of VA Streamline Refinance loans:

- Change your current interest rate

- Change your current mortgage terms

- No down payment required

- Most lenders will allow closing costs to be rolled into the loan

- Reduce monthly payments

VA IRRRL Cons

As with any loan, you should know that while a VA Streamline Refinance loan doesn’t have cons necessarily, you will have to pay closing costs and funding feeds again.

And, your loan “restarts” back at 30 years regardless of how many years you’ve already paid. This isn’t necessarily negative, because it allows you to have smaller monthly payments.

Make sure you also talk to potential lenders as their fees will vary from lender to lender. This will give you the most accurate number possible and help you decide which lender works best for you.

How Do I Get an IRRRL Loan?

If you have any questions when getting an IRRRL Loan, reach out to us at Hero Loan so we can guide you through the process.

1. Check IRRRL Requirements

With a VA-backed loan, there are always going to be certain requirements that have to be met in order to be approved by the VA to individual lenders.

The main requirements are that you currently have a VA mortgage and that you are refinancing to change your current loan terms in one way or another.

And the same requirements to get the initial VA mortgage loan apply to the VA IRRRL.

VA Home Loan eligibility requirements include:

- Current duty status

- Length of service

- Manner of discharge

For those who are still active-duty members, their service history should include:

- At least a 2-year enlistment term for regular members

- At least a 6-year enlistment term if you are a National Guard or Reserve member

- 90 days of active duty during wartime

- 181 days of active duty during peacetime

Other considerations are whether you have a service-related disability, as it may affect the final decision on your VA Loan. Additionally, you must have or meet the following:

- Certificate of Eligibility (COE): Proof that you meet the VA’s requirements for a loan based on your service record. Surviving spouses must still apply for one should they be looking to secure a loan on their own.

- Lending Requirements: While it will vary per individual and lender, a good credit score would be 620 and above. Additionally, aim to have a debt-to-income ratio (DTI) of around 41% to have the best odds.

Since these were required for your original VA Loan, half of the requirements should already be met going into the refinance loan application process!

2. Make Sure You Qualify

Once you know you meet all of the requirements for a VA Streamline Refinance, you then have to make sure that you qualify for the loan. There are certain criteria that have to be met, including:

- It has to be at least 270 days from the closing of your original mortgage

- You must have made at least six consecutive monthly payments on your current mortgage

- There must be at least 210 days between your first mortgage payment and the closing of your streamline refinance loan.

You’ll also have to find the lender that you want to work with and go through their unique qualification process. Every lender is going to differ as far as their credit score approval, the loan application process, and overall qualifying criteria.

3. Prepare Documentation

Knowing what documents to submit, getting all of the documents together, and preparing all of them can be overwhelming, to say the least. And nothing is more frustrating than getting denied due to insufficient documentation.

At Hero Loan, we help you understand all the ins and outs of the VA Loan process and work with you through every eligibility requirement–and do all the paperwork–so you can close in as little as 14 days.

4. Contact Hero Loan

This can really be the first step in the process of getting a VA IRRRL so you can work with a specialist from day one.

Reach out to Hero Loan today to get started with your VA IRRRL application process — or get started on our 5-Minute Loan Approval* form right now!

5. Get your IRRRL!

Hero Loan can help you every step of the way. With experts that are trained and experienced in all aspects of VA Loans, Hero Loan is sure to bring value to you in your journey to refinance your VA mortgage loan.

The Best VA IRRRL (or Streamline) Loan Program

All lenders are going to have their own loan qualification requirements outside of those set by the VA. But for the all-around best VA IRRRL loan program, Hero Loan offers an unmatched experience. From the helpful customer support to the competitive rates offered, you will find everything you need — plus some — at Hero Loan.

Reach out to a Hero Loan representative today so we can help you refinance. Or start our loan application right now!