Free VA Refinance Calculator for VA Loans

- Lowvarates.com Review - September 8, 2022

- USAA Review - August 16, 2022

- Veterans First Mortgage Reviews - August 5, 2022

All veterans, active duty service members, and their spouses can take advantage of VA-backed home loans. Not only are there VA mortgage loans available, but there are also VA refinance loan options.

To make it simple, Hero Loan offers a VA refinance calculator that factors every variable and allows you to see what your monthly payments will be with the current VA mortgage rates.

Table of Contents

What is a VA Refinance Calculator?

A VA refinance calculator is a tool that can be used to show the comparison of your current home mortgage loan to a new refinance loan. The calculator will end up with two results, the first being your new monthly payment compared to the current monthly payment and the second is the total amount of money that you will save over the life of the loan if you were to refinance.

This information is calculated by inputting the following information about your current loan:

- The remaining balance on your current loan

- The interest rate on your current loan

- Your current monthly payment

That information is then compared to the following information about the new loan:

- The interest rate on the new loan

- The term of the new loan

- Closing costs for the new loan

Finally, the calculator will take all of the information that you have provided about both the current loan and the new loan and give you a breakdown of the monthly payments and overall cost of the loan over the full term.

Benefits of using a VA Refinance Calculator

Using a VA refinance calculator provides valuable information that can help you make an informed decision when considering refinancing. You have to also decide whether you would like to use a VA IRRRL or a VA cash-out refinance loan.

After you have decided on which loan to use, you can then find a lender and use the VA refinance calculator to determine the potential benefits of refinancing.

The VA refinance calculator will allow you to choose the best lender to work with by showing the term breakdown using the rates each lender is offering. You will also be able to see if it is worth refinancing now or waiting until interest rates drop some more by showing not only what your new monthly payment will be but also how much you will save over the full term of the new loan.

VA Refinance Calculator:

VA Refinance Calculator Terms

The first set of terms are for the current loan.

Remaining balance

The amount of money remaining on the loans that you would like to refinance.

Interest rate

Your current average annual interest rate for the loans you would like to refinance.

Monthly payment

The monthly amount you currently pay on your loans.

The next set of terms are for the new loan.

Interest rate

The average annual interest rate of the loans you would like to refinance.

New loan term

The amount of time you have to repay your loan.

Closing costs

Typical fees include application fees, appraisal fees, and other (sometimes optional) expenses. You can generally plan on paying around 0.5% to 5% of your refinance amount in closing costs.

VA Refinance Fees & Costs

One of the most important factors to consider when refinancing is the fees and costs that are required. These costs are going to vary depending on which loan you decide to use.

There are two types of VA refinance loans to choose from: an IRRRL or a cash-out refinance loan. Both loans carry the same costs and fees, but differ in the amount required for each one.

What is the VA Funding Fee on a Refinance?

The one unique fee that you will have with any VA Loan is the funding fee. This is a one-time fee paid to the Department of Veterans Affairs. Whether you are refinancing or taking out your original mortgage loan, you will have to pay the funding fee at the closing. (But, there’s no VA mortgage insurance!)

For a VA IRRRL, the funding fee is 0.5% of the loan amount. As for the VA, cash-out refinance loan, it is 2.3% for the first time and 3.6% for all future uses.

The funding fee can be paid upfront at the closing or it can be rolled into the loan amount. It goes toward the VA’s guarantee to lenders that they will cover a portion of the loan should the borrower default on it.

Are There Closing Costs on a VA Refinance?

There are closing costs on VA Refinance Loans just as there are with any other loan. These fees will vary slightly depending on which VA refinance loan you are using and which lender you go with, and can include:

- Funding fee

- Appraisal fee

- Lender origination fee

- Title fees

- Attorney fees

While there are other expenses associated with refinancing it is best to find a lender and speak to them regarding specific requirements. You can expect to pay around 3%-5% of the loan amount on closing costs.

There are some optional costs such as mortgage points or rate discount points. This is a fee that you can pay upfront in exchange for lowering your interest rate. One whole discount point is equivalent to 1% of your loan value and some lenders will allow you to purchase partial points. The more points you buy, the lower your interest rate will be.

VA Refinance Rates

VA refinance rates are in the same ballpark as current VA mortgage rates. Typically, VA cash-out refinance loans will carry a slightly higher interest rate than a VA IRRRL. You can expect to have the lowest possible interest rates available with a VA loan.

There is also the option of paying mortgage points in order to lower the interest rate more than what is being initially offered. It will depend on the lender that you are working with, they all offer different rates and terms.

How Soon Can You Refinance a VA Loan?

If you are looking to refinance with either a VA IRRRL or a VA cash-out finance loan, you will have to make at least six consecutive monthly payments on your current mortgage before you are eligible to refinance.

There has to be at least 210 days from the date of your first mortgage payment prior to refinancing the loan. These are general rules that will carry over to any lender, however, every lender may have their own set of requirements on top of that for you to meet prior to refinancing.

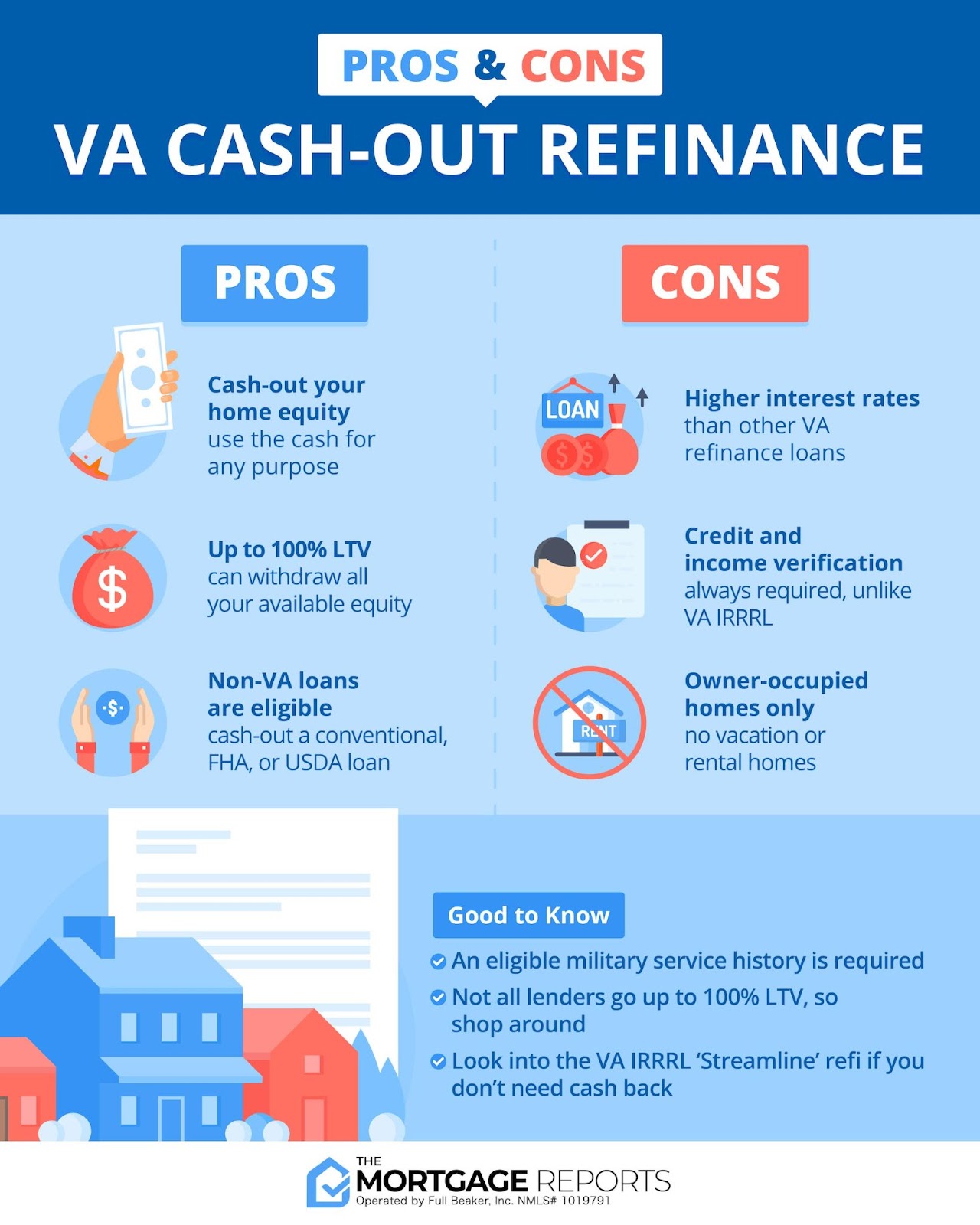

VA Streamline (IRRRL) vs. VA Cash-Out

The two types of VA refinance loans are the VA interest rate reduction refinance loan or streamline refinance loan and the VA cash-out refinance loan. You can see the key features and differences below.

VA Streamline (IRRRL)

Features

- Can only be used on current VA mortgage loans

- Doesn’t have to be primary residence as long as it was at one time

- 0.5% funding fee

- No appraisal required

- Cannot take cash out

Why choose a VA Streamline Refinance Loan?

- Lower interest rates

- Change loan terms

- Switch from an adjustable-rate mortgage (ARM) to a fixed-rate loan

VA Cash-Out Refinance Loan

Features

- Can be used on non-VA loans

- Must be the primary residence

- Pull cash from the equity in the property

- Regular VA funding fees apply. 2.3% first use, 3.6% all future uses

Why choose a VA Cash-Out Refinance Loan?

- Make home improvements

- Consolidate private loan debt

- Lower interest rates

- Change loan terms

More VA Loan Calculators for…

Make life easier when it comes to your VA Home Loans with one of the several different calculators that can be found on the Hero Loan website. These can give you an accurate picture of what can be expected before applying for a loan or while paying off a loan.

VA Loans

When it comes to a basic VA home loan, the best way to pay down the loan is to make extra payments. This will shorten the life of your loan and save you a ton of money in the long run.

Using a mortgage payoff calculator can help you determine how much you will save depending on how you decide to add those extra payments.

Three ways to make extra payments are:

- Lump sum payment

- Paying more than your minimum each month

- Setting up bi-weekly payments

If bi-weekly payments sound like something you can handle, there is a bi-weekly mortgage payment calculator to help you determine the payments and savings from switching. Regardless of which method you choose, it will pay off in the end.

Home Equity Loans

If you need to explore a home equity line of credit (HELOC), it’s important to understand that the VA does not back these loans or offer any assistance with them. This will be dependent on your creditworthiness as defined by the lender.

While the VA does not offer a HELOC you can still apply for one if you have a VA mortgage loan. You can refer to Hero Loan’s HELOC payoff calculator to determine if it is worth pursuing.

Cash-out Refinance

For eligible service members that need to take out some cash on the equity of their home however they don’t want to go the conventional route of a home equity line of credit, the VA offers a cash-out refinance option.

As opposed to just being another line of credit you have to actually refinance your current loan however you are able to take cash out against the equity that you have in your home up to 100% loan-to-value ratio.

If a VA cash-out refinance loan is something you are considering, be sure to first check out the cash-out calculator which will give you all the information you need using the rates and terms provided by your lender.

Is a VA Refinance Worth It?

It’s a matter of your personal financial situation that will determine whether a VA refinance is worth it for you. In many cases, you will absolutely benefit from a VA refinance, and you can use the calculator and all of the information in this article to see that.

To help you determine whether it is worth it for you, reach out to the team at Hero Loan for their expertise. They will be able to walk you through the process from start to finish with all of the details you need to make an informed decision.

At Hero Loan, we work with service members looking to buy or refinance a home on a daily basis. Start by going online and filling out our loan approval application today. There is a VA home loan expert waiting to help you right now!