Can I Get a VA Loan with a 600 Credit Score?

- Lowvarates.com Review - September 8, 2022

- USAA Review - August 16, 2022

- Veterans First Mortgage Reviews - August 5, 2022

For many veterans and active-duty service members, a VA loan could change their lives. With no down payment required, competitive interest rates, and flexible qualifying criteria it may be the only option for some looking to buy a home.

And because The U.S. Department of Veterans Affairs guarantees a portion of the loan, it’s appealing to lenders as well. This is what makes VA Loans a unique opportunity for both the lender and the borrower.

The question is, however, how flexible is the qualifying criteria exactly? Can you still be approved for a VA loan with a 600 credit score?

If you happen to have a credit score of around 600, we’ll provide you with all of the information that you need to know prior to applying for a VA loan.

Table of Contents

VA Loan Minimum Credit Score Required for Approval

The U.S. Department of Veterans Affairs does not require a minimum credit score for the VA loan. Instead, the credit score requirements are set by the individual lenders that are offering the loan.

Because service members don’t always have time to build a solid credit history, this can give them a disadvantage when it comes to applying for a loan. That’s why VA Loans offer flexible qualifying criteria as well as competitive mortgage rates that give service members a chance to afford what they otherwise wouldn’t be able to with a conventional loan.

The VA does advise lenders to use their best judgment to determine who is eligible for a VA loan, and often the minimum credit score typically ranges from 580-620. Naturally, if you can boost your credit score prior to applying for a loan it will improve your chances of obtaining one.

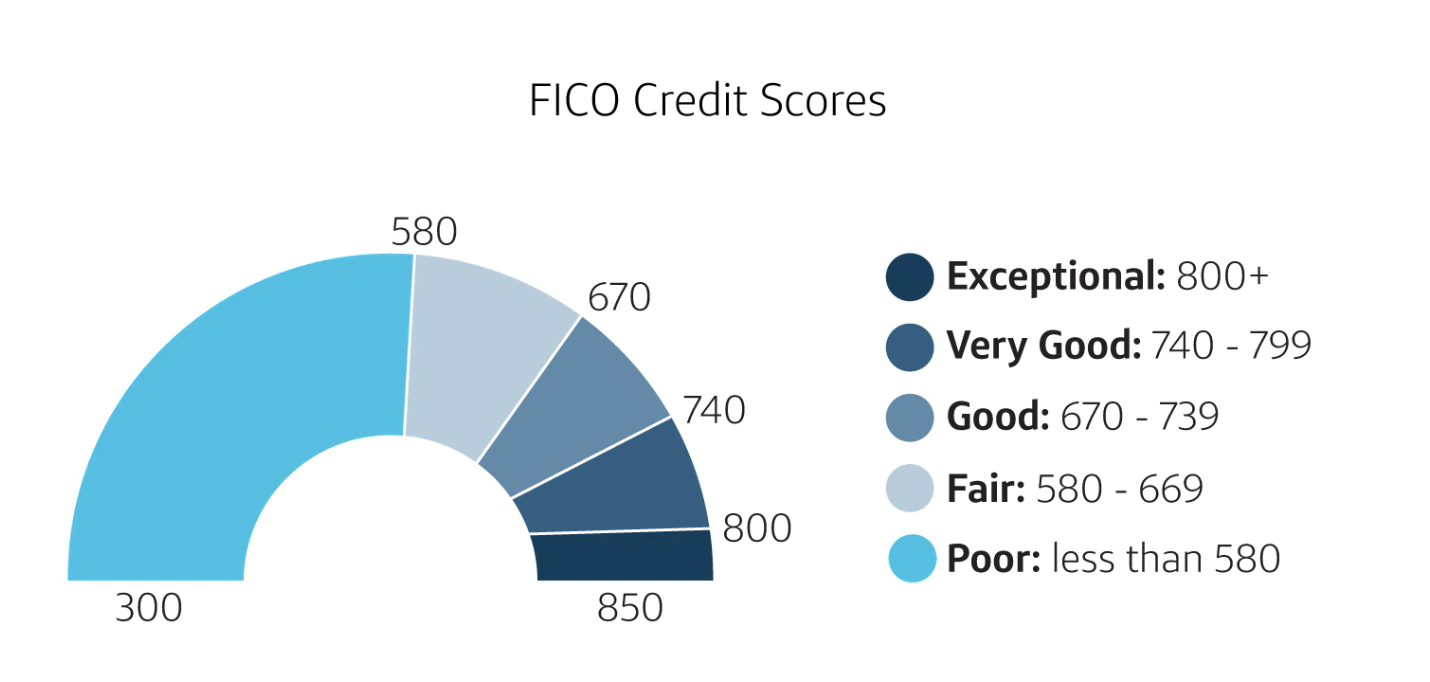

Where does a score of 600 fall on the credit spectrum?

Every credit scoring company has its own interpretation of the credit spectrum.

For example, Fico considers any score from 300-580 as poor and any score from 580-669 as fair:

VantageScore considers any score from 300-500 very poor and anything from 500-600 poor.

Regardless of which credit reporting agency provides your score, 600 is a lower score. But if you look at it as only being 100 points away from being a “good” credit score, then you’ll see it’s an attainable benchmark!

Credit scores are always changing, so it’s important to keep tabs to ensure there are no reporting errors and that you’re not making any simple mistakes that can be avoided. This will keep you from falling below your 600 credit score, and even help you improve it.

How Can a VA Loan 600 Credit Score Affect a VA Loan Approval?

Much like any other loan, a credit score of 600 or less can make it more difficult to obtain a VA loan. Credit lenders want to see that the borrower will be able to pay back the loan and not default. Statistically, those with lower credit scores have a much higher chance of defaulting on their loans.

Credit scores are a reflection of your past money borrowing and repayment history. If you were perfect as far as paying back everything you’ve ever borrowed on time, then you would have an excellent credit score.

When you have a low credit score this tells the lenders that you’ve had issues in the past with paying back your loans on time, which makes it riskier to provide you a loan today.

There are ways to improve your credit score as well as ways to convince lenders of your worthiness regardless of a low credit score. Knowing what to expect and how to handle it will get you one step closer to securing the loan you need.

How to Mitigate a 600 Credit Score When Applying for a VA Loan

There are steps that you can take to mitigate a low credit score if you are looking to apply for a VA loan. Even though all lenders look at your credit score, they will also take into consideration your whole financial situation.

Unfortunately, credit scores can be affected by factors outside of your control such as fraud or reporting errors. In these cases having proper documentation and proof of funds could be the difference between getting a loan and not.

The following list of tips will help you to mitigate your credit score right away.

1. Raise your credit score

Raising your credit score is always the first step in the process. This won’t happen overnight, so don’t be discouraged when you don’t see any improvement after a week or two of working on it.

But if you continue to work on improving your score it will start to happen and lenders will respond to this.

There are many ways to raise your credit score that just take a conscious effort on your part, and we’ll go into more of that next.

2. Use a co-signer

When time is not on your side and you need to move fast on a loan, you can use a co-signer. This is someone that has a good financial standing and is willing to sign on to pay for the loan should you be unable to.

For a VA loan, the co-signer is required to be either a spouse or another eligible military service member. This can be a good option to get you started without having to wait for your credit score to rise.

3. Utilize cash

If you have a significant amount of liquid cash to use it could ease some of the worries that lenders have regarding your lower credit score.

This goes back to looking at the whole picture. If you have a low credit score, but also have a high monthly income and a significant amount of money for a down payment, the lender is much more likely to trust you with their money.

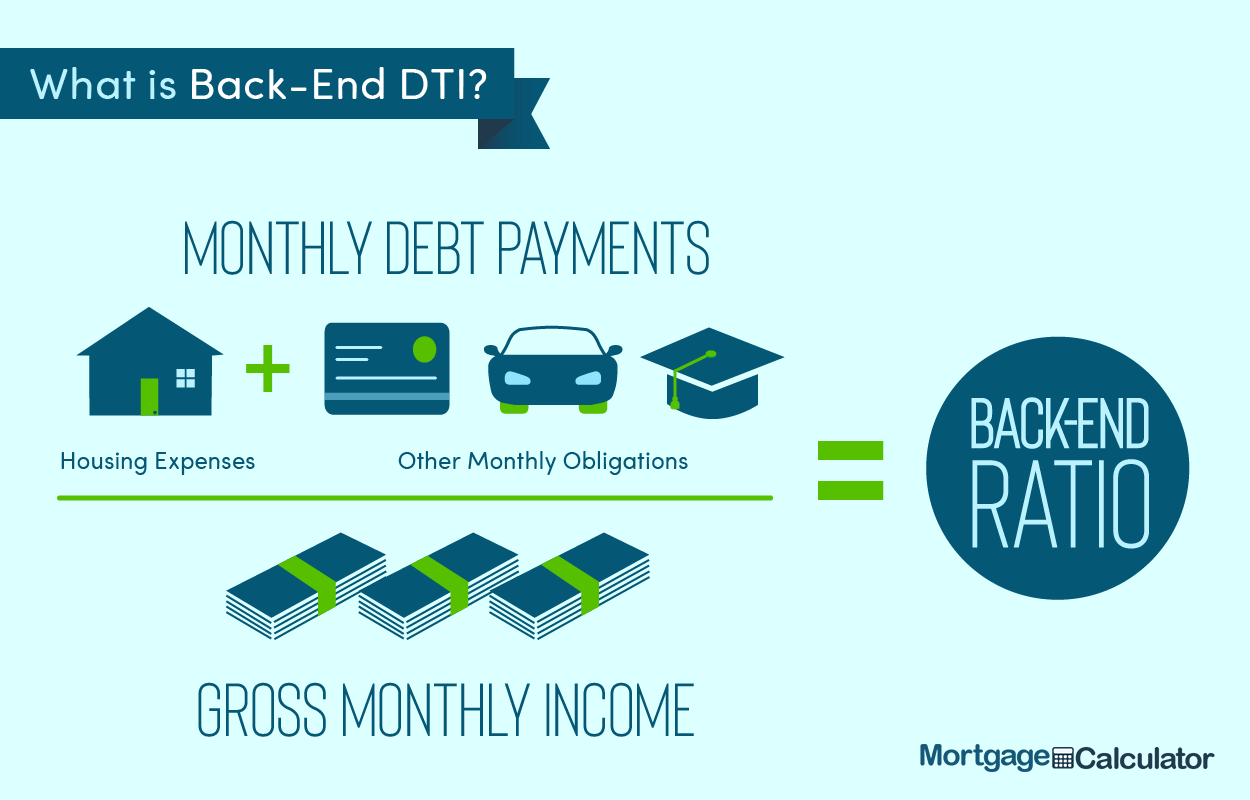

4. Lower your Debt-to-income ratio (DTI)

One of the main factors that lenders will focus on is your debt-to-income ratio. This is the percentage of what you make each month that goes to what you owe each month, or your monthly expense divided by your pre-taxed income.

So the more that you make and the less you owe, the lower your DTI ratio.

Most lenders want to see a DTI ratio of 43% or lower. This will vary from lender to lender however it is rare to see a borrower get approved for a loan with a DTI ratio higher than 43%.

Ideally, you want to be at a 36% or lower DTI ratio with no more than 28% of your debt going towards paying a mortgage or rent.

How to Improve a 600 Credit Score for a VA Loan

So what are some ways to improve your credit score? Here are a few tips to get you started.

Review your credit reports

Looking up your credit reports will give you insight into what exactly is affecting your score. Even if you think you know what is causing the low score, there could be some items — like applying for a credit card — that can impact it.

Some items that might cause your credit score to drop include:

- You have late or missing payments for loans or credit cards

- Your credit utilization has increased

- Your credit limits has decreased

- You recently applied for a mortgage, loan or new credit card

- You closed a credit card

- You’ve gone through a major financial event

Similarly, if your loan application is denied you’ll want to review the adverse action letter you’ll receive. This will tell you exactly why you were denied the loan.

Having this information will allow you to come up with a clear plan in order to fix any issues that are causing your credit score to stay at a lower number and ultimately getting you denied the loan that you are applying for.

Have inaccurate reporting removed

Even on official credit reports there can be false reporting and errors that affect your credit score that were not your fault.

You can have these errors removed from your credit report in order to boost your score. Note: it still takes time for your credit score to boost back up after an error.

Pay more than the minimum every month

Every creditor will give you a minimum amount due per month which will depend on how much money you borrowed.

You don’t have to pay any more than the minimum payment, however, credit bureaus like to see that you have the ability to pay more than you’re asked to pay.

Use your credit cards

Using your credit card — and paying for your credit card in a timely manner — is an easy way to boost your credit score. Creditors want to know that you are going to take the money they are offering as long as you can pay it all back.

Someone who carries a balance each month but pays more than the minimum payment will have a better score than someone who doesn’t use their credit cards at all.

Set up automatic payments

You have the option to set up automatic payments for any bills that you have, from rent to utility bills to auto payments. This is the best way to ensure you never miss a payment, and missed payments can be a huge issue for your credit score.

Late payments are a very common problem for those with lower credit scores. It directly impacts your credit score and it is also one of the easiest things to avoid. By setting up automatic payments, you’re ensuring that the payments are being made on time no matter what you might have going on in life that might distract you from making the payment on your own.

Can You Get a VA Loan with a Credit Score of 600?

There’s no straight answer here: it’s possible that some lenders will approve you for a VA loan with a credit score of 600, but it’s going to vary from lender to lender. So finding the right VA lender that can help you through the process will be a huge help.

Hero Loan offers VA loans, loan experts, and a comprehensive list of resources to help you through the process of obtaining a VA loan. Our VA loan representative who will meet you at your financial location based on your current credit score and other influential monetary records to find a financial solution that suits their home buying needs. Hero Loan’s professional and efficient services can help our clients qualify for a loan in minutes, with closing periods in as little as 14 days.

Don’t put your life on hold due to a 600 credit score. Hero Loan has a fast and easy process to get you on your way to securing a VA loan today. Start by filling out our loan application. You’ll be in the best position possible with Hero Loan guiding you through the process.