VA Loans for First-Time Homebuyers [2024 Guide]

- Lowvarates.com Review - September 8, 2022

- USAA Review - August 16, 2022

- Veterans First Mortgage Reviews - August 5, 2022

Homeownership is something that most people aspire to eventually achieve. From the day you move out of your parents’ house and start to live your life on your own for the very first time, you might hope that you’ll be able to purchase a home of your own someday instead of having to rent a place.

And one of the first steps to being a first-time homebuyer is finding a great loan to fit your needs. If you’re either an active-duty service member or a military veteran, a VA Loan might just be the best fit for you. If you’ve been weighing the pros and cons of a VA Loan as a first-time homebuyer, then it’s time to understand how to take advantage of the incredible VA Loan options in this country.

Table of Contents

What are VA Loans?

VA Loans are similar to Conventional Loans in many ways: you borrow money from a private lender so you can buy yourself a primary residence in your home state. Unlike regular mortgages, however, VA Loans are guaranteed by the US Department of Veterans Affairs.

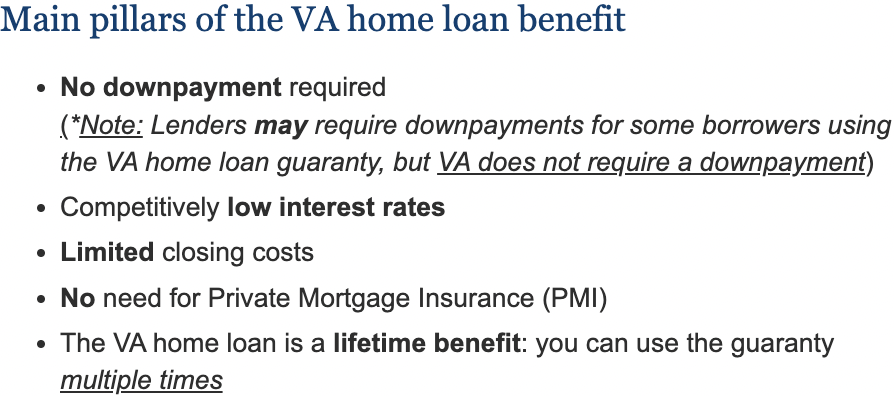

In other words, the government will pay for your down payment in advance, and you won’t need to shell out a huge amount of cash before getting a house, because there is often 0% down payment required for VA Loans.

Advantages of VA Loans

One great advantage of taking a VA Loan is that private lenders tend to favor these more than regular mortgages. Plus:

- There’s 0% down payment required

- You often a lower interest rate

- Underwriters place less stringent qualifications

- There’s no need for private mortgage insurance (unless you really have to)

The VA Loan is, in fact, one of the hard-earned benefits of a soldier’s active duty for the United States. In a way, it’s part of our country’s way of saying “thank you for your service” – like having access to healthcare or financial assistance, or even receiving VA disability benefits.

Source: U.S. Department of Veteran Affairs

Can first-time homebuyers get a VA Loan?

As long as you have a strong credit history and can afford to pay off your debt, you probably won’t get denied for applying for a VA Loan (or two!), even if you are a first-time homebuyer.

Fortunately, your credit score and employment status are only one piece of the puzzle, and the lender generally takes a look at the entire picture, rather than just one or two variables.

In fact, even folks who have declared bankruptcy in the past can still get a VA Loan. Sure, you might need a cosigner for the loan, but that’s not a dealbreaker. It’s there for all veterans to take advantage of.

How To Get a VA Loan for Your First Home

For the first-time homebuyer, getting a VA Loan may seem like a lot of effort at a glance. You might even be wondering if it’s really as great as it seems, or if it’s too good to be true. The fact is, these are fairly common misconceptions about VA Loans.

The biggest thing that you need to be aware of when getting the ball rolling on your first-time homebuyer VA Loan is that there are a few things you’ll have to do on your side to start the process.

Fortunately, it’s very straightforward. And if you have a great mortgage lender, like Hero Loan, it will be even easier. Hero Loan will do every step of this process with you:

- Get a COE (Certificate of Eligibility)

- Secure a Mortgage Lender (unless you’re working with Hero Loan, in which case we’ll help you with your COE)

- Get Pre-Approved

- Find a Real Estate Agent

- Buy Your First Home

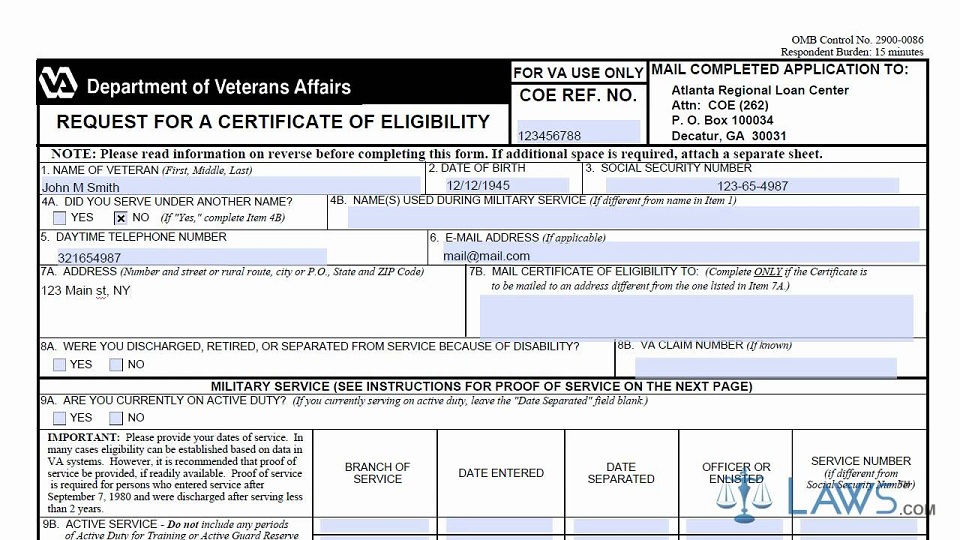

Get a VA Loan Certificate Of Eligibility

Before you do anything else, you should start step one to make sure you’re eligible for a VA Loan. At Hero Loan, we’ll help you obtain this paperwork and apply for your COE (not to mention we’ll do all the paperwork for you throughout the VA Loan process).

Source: VA.gov

To get a COE, there are a few things you need to know. These include:

- Your current duty status

- The overall length of service

- And the character of service

Other than the regular 90- and 181-day length of service requirement, the Home Loan Expert also makes sure that you’ve served for:

- At least 2 years if you are a regular service member

- At least 6 years if you are a member of the National Guard or a Reservist

Another consideration that might affect the final decision is whether or not you have a service-connected disability. In addition to that, they also have a couple of other lending requirements. Normally, they look for these three things:

- Credit Score: Generally, they take a 620 credit score as the ballpark range for getting approved. If yours is any better than that, then you’re more likely to get your VA Loan.

- Certificate of Eligibility (CEO): This allows them to know that you’ve checked all the necessary boxes to satisfy either the military service or the surviving spouse requirements. With that in hand, you’ll be more equipped to get approved for the VA home loan that you want.

- Debt-To-Income (DTI) Ratio: Your Debt-To-Income ratio should be right around 41% or (ideally) lower. If you seem to have a good stream of residual income, you may be allowed to get by with a little bit higher DTI than that.

Plus, all veterans need to have been honorably discharged through one of the following means:

- Service-connected disabilities

- Military hardship

- Military downsizing

- Government convenience

- Medical conditions that render a soldier unfit for duty

- Retirement

- Early out

Unless you have a huge blemish on your record that nets you a bad conduct discharge (or worse, a dishonorable discharge), then you are probably eligible for a VA Loan. This is especially true if you already currently get any other veterans’ benefits.

If you’re curious to determine your eligibility, you can always request your documents electronically via the VA’s web portal. The information included therein can let you know if you’re eligible for a first-time homebuyer VA Loan or not. Or, reach out to us at Hero Loan so we start the process for you.

Find a Mortgage Lender

Next up, you’ll need a mortgage lender. What most people might not realize at first is that the Department of Veterans Affairs does not actually issue mortgages. Instead, it relies on banks and private mortgage lending companies to provide the mortgage services and interest rates.

For the first-time homebuyer, this step could be a little confusing. It’s best if you consult a reliable mortgage company about your case first, especially one that has experience working with veterans like yourself. At Hero Loan, our VA Loan program makes it easy for Veterans and military families to get the home loans they deserve.

We help you understand all the ins and out of VA Loans, including how they work, why you should (or shouldn’t choose one) how to get one, and even if there are better loan options for you, like Cash-Out Refinancing, FHA Loans, or even Conventional Loans.

Get Pre-Approved

The pre-approval process for a first-time homebuyer VA Loan is almost completely no-fuss, and it’s a process that gets as objective as it can. You’ll primarily be asked about your current income, how much in savings you currently have, your credit score, and other details that help the mortgage lender gauge how much you could pay in the future.

The same principles for a regular mortgage pre-approval apply here. You need to remember that it’s not a within-the-day kind of thing that you’d get in one meeting with the lender. On average, the pre-approval process for VA Loans could take almost two months, or as little as 14 days with Hero Loans–even though closing VA Loans can take a little bit longer when compared to a Conventional Loan.

Once your mortgage lender has gone through any information provided by your records and forms, they’ll tell you whether you can realistically get that loan–as well any funding fees.

Find a Real Estate Agent

Now, finding the best real estate agent for your home purchase is a somewhat personal choice. However, it’s strongly recommended to get in touch with one if possible. The reason for this is because a real estate agent acts as the liaison between you, as the homebuyer, and the seller that you’ll buy your new home from.

Real estate agents know all the houses being sold in their area and can help break down which neighborhoods are in high demand and other considerations. Plus, a good real estate agent knows which houses are good, and which ones might not be the right fit for your needs.

A real estate agent also sets up escrow accounts so you can be sure that your money won’t just suddenly disappear in a home-selling scam. You would also want their help when it comes to picking home-services providers, as they know all the neighborhoods that offer the amenities and other things you’re looking for.

Just know, home appraisals can be a little tougher for VA Loans because the VA needs to ensure homes purchased by veterans and active-duty service members are fiscally and structurally sound.

Start Shopping for Your First Home!

After you’ve decided on an agent, picked out a mortgage lender, received your pre-approval papers for your first-time homebuyer VA Loan, and have gotten a Certificate of Eligibility, it’s time for the fun part–picking out your first home!

And of course, take advantage of all the support from your real estate agent and mortgage lender you can in this part of the process.

Best VA Mortgage Lenders for First-time Homebuyers

With so many options out there to choose from, trying to narrow down the best mortgage lender for a VA Loan as a first-time homebuyer can be a headache. If this is your first foray into trying to sift through all the different lenders with all their different rates and policies, you’ll likely run into two problems:

- It’s gonna take you a while.

- You’ll be doing a lot of asking around.

To spare you the effort, here are three of the best VA Loan mortgage lenders in the United States!

Hero Loan

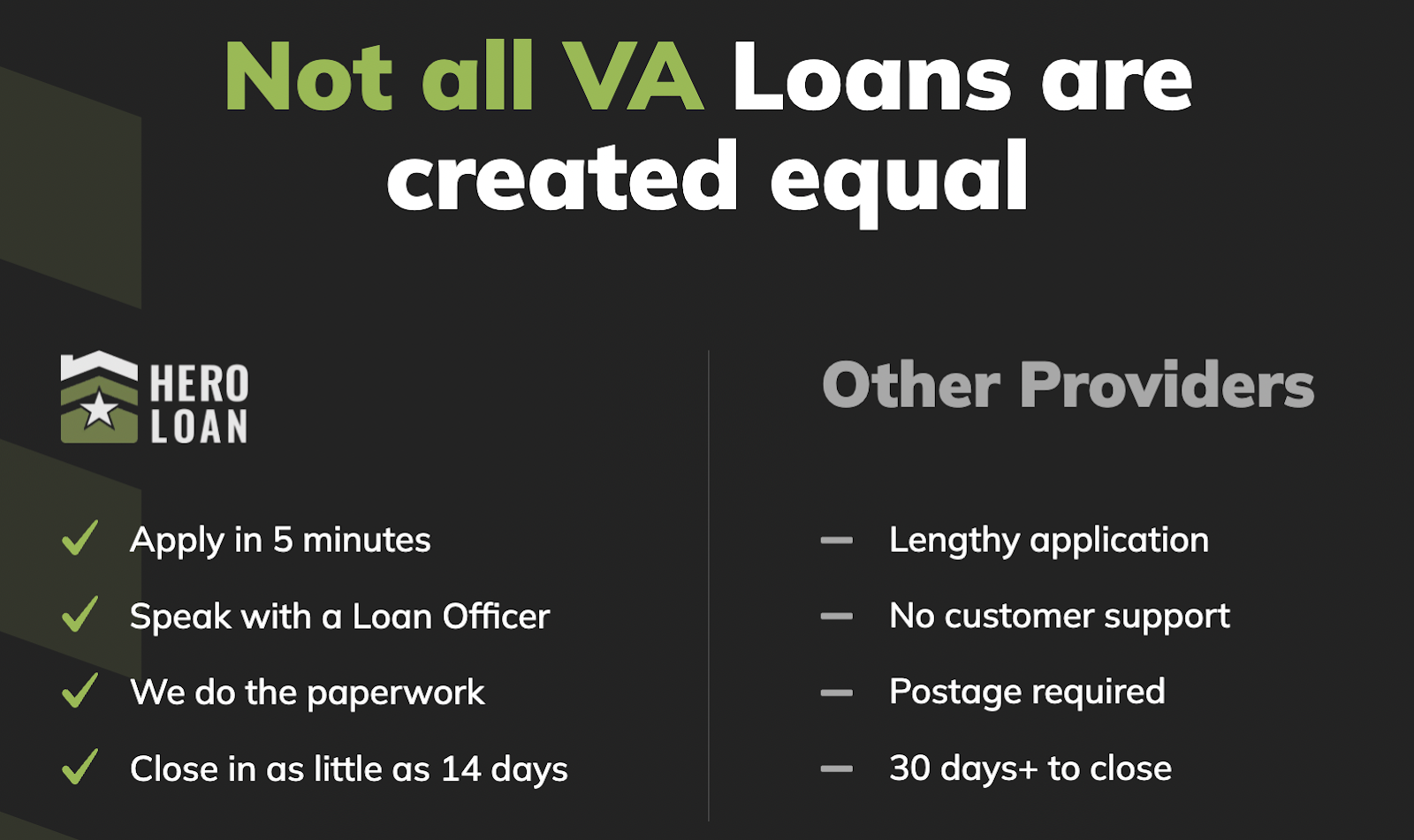

As one of the fastest-growing mortgage lending platforms in the country, Hero Loan proudly serves active-duty military personnel, veterans, and their families. This mortgage lender strives to help ensure that veterans who are looking for a loan get prompt, personalized service, and they genuinely love working with those who have selflessly given so much for their country.

Unlike other mortgage lenders, which can take as high as 60 days, Hero Loan is a direct-endorsed VA Lender. This means that they can help you close on a VA Loan in as little as 14 days. To make things as easy as possible for you, they also underwrite all VA Loans in-house, allowing you to enjoy lower mortgage rates. You won’t have to worry about upfront or out-of-pocket costs, either–and yes, that also includes the appraisal!

How It Works:

Hero Loan has an enticing roster of loans and services that they offer. Apart from the standard VA Loan, some of these also include:

- VA Streamline Refinancing

- Conventional Loan Refinancing

- VA Cash-Out Refinancing

- FHA Loans

You can use the Hero Loan website to fill out a few preliminary details and apply for the loan or service that you’ve chosen, or let them know you’re not sure. From there, a loan officer will be assigned to you who will take you through the minutiae and explain the details of the loan that you are about to borrow, or how to choose the right one for you.

They’ll also help you get the all-important VA Loan Certificate of Eligibility (COE) and fill out all the VA paperwork for you. After you’ve sorted out the necessary details, all that remains for you to do is wait until the loan closes.

But don’t worry about having to wait too long–for most active-duty servicemembers and veterans, getting your VA Loan approved through Hero Loan can take as little as 14 days (compared to the standard two months)!

Pros:

- Fast loan approval

- They do all the VA Loan paperwork in-house

- In-house underwriter

- No out-of-pocket fees

Cons:

- Services only military personnel, veterans, and their families

The Home Loan Expert

If you’ve been thinking about buying a home and you’re trying to get started on a VA Home Loan in the US, then The Home Loan Expert are the folks you want to talk to.

With their famous 5-Minute Loan Approval* application, you can get your loan approved with ease.

Apart from VA Loans, though, The Home Loan Expert also features a seamless online experience and a bounty of other options for mortgages and home loans. This mortgage lender is ready to be your go-to guru when it comes to buying a house.

Even better, The Home Loan Expert completely understands that the process of getting your first mortgage can be a tough, which is why they’re committed to keeping the process as straightforward as possible.

In addition to VA Loans, The Home Loan Expert also offers:

- Adjustable-Rate Mortgages

- Bank Statement Mortgages

- Cash-Out Refinances

- Conventional Loans

- Debt Consolidation Refinancing

- FHA Loans

- A First Responder Loan Program

No matter what your needs are, The Home Loan Expert just might have the exact loan you’re looking for!

Pros:

- Options of VA Interest Rate Reduction Refinance Loans or Cash-Out Refinancing

- Access to the Native American Direct Loan program (if needed)

- House grants can be adapted for those of you with a disability

- A VA home loan calculator to help you crunch those numbers

Cons:

- It’s incredibly tempting to want to consider a different loan from their robust offerings, rather than the VA home loan that first caught your eye

Veterans United Home Loans

As a prime direct mortgage lender, Veterans United Home Loans is well versed in everything to do with loans. Sure, they do specialize in VA mortgages, but they also know their way around USDA, FHA, jumbo, and conforming mortgages.

How It Works:

Let’s say you want to refinance a VA mortgage home loan. In that case, you can choose between a:

- VA IRRRL (Interest Rate Reduction Refinancing Loan), which is used to convert an ARM to an FRM, or to reduce the interest of the borrower

- Cash-Out Refinance

Unlike a lot of other lenders, when applying for a VA Loan through Veterans United Home Loans, you’ll be able to apply for mortgage credit data (which is not to be confused with your primary credit data). For instance, you could potentially show proof that you usually take care of your bills on time, which can help you possibly secure a lower interest rate – especially if you have a somewhat less stellar credit score.

Pros:

- A good option for people with lower credit score

- Has other loan options apart from VA home loans

- Uses mortgage credit data instead of your primary credit data

Cons:

- While they may have customized loans, they don’t have the more common kinds

- Customized rates are not available when applying online

Conclusion: Choosing a VA Loan as a First-time Homebuyer

Buying your first place is a once-in-a-lifetime experience, and it can be an incredibly special moment for any veteran or active-duty servicemember. Setting down roots and calling a place your home is like little else–which is why it’s so important to familiarize yourself with the ins and outs of a first-time homebuyer VA Loan when you’re finally ready to move forward with your purchase.

That’s why Hero Loan is proud to offer the best customizability and rates for any veteran or active-duty service member, all with the least amount of effort on your side. Their friendly team of professionals is happy to walk you through the entire process from start to finish, making your dreams of becoming a first-time homeowner a reality.

If you’re ready to get your first home and want to start applying for a VA Loan in minutes, why not reach out to Hero Loan today?